Forex Signals US Session Brief, Nov 7 – Risk Flips On and Off on Trade Deal Comments, the BOE Prepares to Cut Rates

The BOE left rates unchanged but 2 members voted to cut then, pointing to a rate cut after Brexit finds a way

The sentiment improved considerably in October in financial markets. The US and China reached a partial trade deal and UK PM Boris Johnson struck a Brexit deal with the EU. As a result, risk assets such as stock markets and commodity currencies have been climbing higher. But, the UK parliament shot dead Johnson’s deal once again and the UK is now heading towards general elections. The “Phase One” trade deal is not so certain now wither, after comments form a senior US official last night.

Last night, we heard a senior Trump administration official say that the partial trade deal could be postponed for December as discussions continue over terms and venue. It’s still possible US – China trade deal pack will not be reached, but a deal is more likely than not. Pushing for more tariffs rollbacks not seen derailing progress toward trade deal. Those comments turned the sentiment negative during early Asian session and safe havens such as GOLD climbed higher, while risk assets retreated. But, China offered to roll back tariffs on US poultry imports early this morning, which flipped the sentiment to the positive side again. The Bank of England left interest rates unchanged but the MPC Official Bank Rate Votes moved close in favour of a rate cut, so the BOE is getting ready to cut interest rates once the Brexit path is clear.

The European Session

- Italian Retail Sales – Retail sales have been mostly negative in Italy this year, declining in three out of the last four months, although August was revised lower to -0.5% from-0.6% previously. But, retail sales were expected to turn positive in September and grow by 0.3%. They turned higher indeed and increased by 0.7% that month, as today’s report showed.

- China Makes Another Move in the Right Direction – The partial trade deal was going well and heading in the right direction, but last night we heard comments from US officials that the deal might be delayed until December. That turned the sentiment negative in forex, but this morning we heard Chinese officials say that China is considering removing US poultry import restrictions. This is a good move, since it would pas the ball to the US court now.

- ECB’s Holzman Sounding Hawkish – The European Central Bank member Holzman commented on interest rates this morning, saying that negative rates currently send the wrong signal. He wants ECB to get rid of negative interest rates ASAP. So, he basically wants to hike interest rates since they are already negative. But, we know he is a hawk, so it’s not a big surprise and the ECB won’t hike rates anytime soon.

- UK Finance Minister Wants to Increase Fiscal Spending – UK Finance Minister Sajid Javid said earlier today that it is a responsible time to invest and the time to do that is now. the first rule will be to have balanced current budget, second fiscal rule will ensure we can invest more but live within our means. Third fiscal rule means that is debt servicing costs rise too much we would re-consider plans. Long term projects like road and rail will not exceed 3% of GDP. We will borrow some more to invest. These are some positive comments.

- German Industrial Production – The industrial production has been declining in Germany this year, just like manufacturing. In the last five months, we have seen production decline three times. Although, October’s report showed a 0.3% increase for August, which was revised higher today to 0.4%. That was a good sign for a probable reversal of the declining trend, but today’s report was expected to turn negative again and show a 0.3% for September. The decline was bigger, at -0.6%, so no trend reversal for German manufacturing.

The US Session

- BOE Interest Rate Decision – The Bank of England left interest rates unchanged at 0.75% as expected. MPC Asset Purchase Facility votes also remained unchanged at 0-0-9 in favour of keeping things as they are. Asset Purchase Facility remained unchanged at 435 billion GBP. But the MPC Official Bank Rate votes changed to 0-2-7 from 0-0-9 last month, which suggest that the BOE is preparing to cut rates, but not before we know what will happen with Brexit.

- BOE Inflation Expectations – The Bank of England released inflation expectations, together with the interest rate decision. Inflation has been revised lower for three years. In one year’s time, the CPI is estimated now at 1.51%, down from 1.90% in August, in two years time inflation was revised down to 2.03% from 2.23% in August and in three years time inflation expectations were pulled down to 2.25% from 2.37%.

- BOE Press Conference – BOE’s Carney held a press conference after the rate decision. He said that the recent Brexit deal creates a possibility of a pick up in UK growth. World risks is slipping into low growth, low inflation. Although, many of these dynamics occurred first in the UK. Both reduced Brexit uncertainty and stronger world economy assumed in BoE forecasts, but neither is for certain. Now we have evidence that UK households are doing precautionary saving before Brexit. Brexit uncertainties are weighing particularly heavily on business investment. Chances of a no-deal Brexit scenario have been reduced and it has pushed up the GBP. The pick up in UK growth is likely to be limited by a lack of supply capacity in the economy. New BoE Brexit assumptions assume transition occurs over 3 years vs previous much longer transition. This will be enough to reach a trade deal before Brexit is finalized.

- US Unemployment Claims – The US unemployment claims report was released a while ago and initial jobless claims came in at 211k against 215k estimated. The previous week was revised higher to 219k from 218k. 4 week moving average moved a tad higher to 215.25k from revised 215k last week. Continuing claims also rose to 1689k versus 1682k estimated. The prior week was revised to 21692k from 1690k.

Trades in Sight

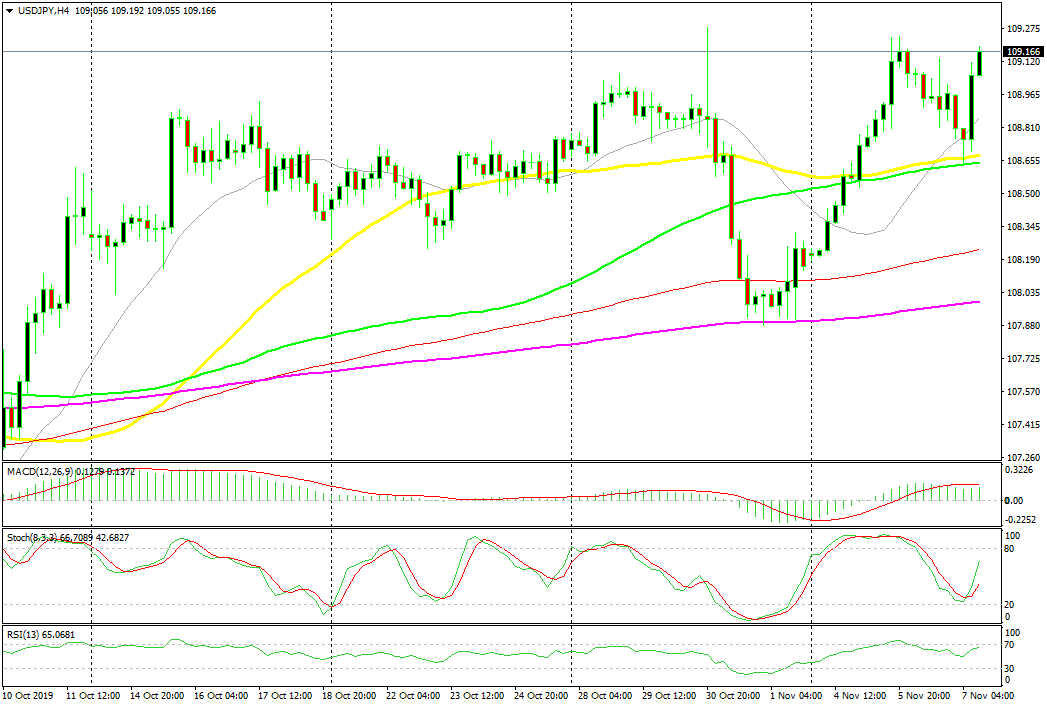

Bullish USD/JPY Again

- The trend has been bullish this week

- The sentiment has improved

- The pullback down is complete on H4 chart

- MAs provided support on the pullback

The 50 and 100 SMAs provided solid support overnight

USD/JPY has turned bullish this week after making a strong bearish move last week, following the rate cut from the FED and the failure to pass the Brexit deal in the British Parliament once again. But the sentiment has improved this week and stock markets have turned bullish again, while safe havens such as Gold and the JPY have turned bearish. USD/JPY retraced higher last night after comments from US officials that the trade deal might be postponed for December. But, the decline ended at the 50 SMA (yellow) which provided support together with the 100 SMA (yellow) and this pair jumped higher.

In Conclusion

The Bank of England left interest rates unchanged today as widely anticipated, but two members voted for a cut, which is a sign that once Brexit is clear, the BOE will start easing, since the UK economy and the global economy are weakening. The USD has resumed the bullish trend of this week, after it retraced lower overnight.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts