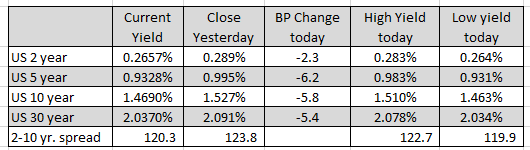

US PCE Inflation Remains Steady in August

Inflation remains high and steady in the US, way above the FED 2% target

The US core PCE data for the month of August remain steady at 3.6%. That was the expected rate as well. Although inflation remains well above the 2% level, the expectations are that some of the gains are transitory and will come down over time. However, the risks still remain to the upside.

Fed’s Mester said today that she expects inflation to remain above 2% next year and the year after. Feds Harker today also talked of higher inflation saying that he’s penciling in a significant risk of higher inflation and that some business leaders are saying there could be years to resolve supply chains.

Personal Consumption Expenditure Inflation Report

- PCE core MoM +0.3% vs +0.3% expected

- Prior MoM +0.3%

- Core PCE +3.6% vs +3.6% expected

- Prior was 3.6% y/y

- Headline PCE +4.3% vs +4.2% prior

- Deflator MoM +0.4% vs +0.4% prior

Consumer spending and income for June:

- Personal income -0.2% vs +0.3% expected. Prior month +1.1%

- Personal spending +0.8% vs +0.6% expected. Prior month +0.3%

- Real personal spending +0.4% vs -0.1% prior

These numbers are largely in line with the consensus but the income line was surprisingly soft. The good news (for the Fed) is that there’s no big surprise jump in inflation.

In other fundamental news today, the ISM manufacturing index came in at a strong 61.1% versus 59.6% but construction spending was unchanged versus 0.3% estimate for the month of August. The Michigan consumer sentiment came in hundred 72.8 versus 71.0 expected. So overall not a bad day as far as economic data goes.

In the markets, there was some support premarket after news that Merck was looking to fast track a Covid drug that would lower hospitalizations by 50% for those infected. That finally sent Merck shares higher but also the stocks like airlines and Disney also surged on hopes for a more normal economy going forward. Will that get people back to work?

Next week we get the US jobs report on Friday with expectations for 490K increase in jobs. That is down from higher levels for the recovery, but would be up from the 235K surprise reading last month. Despite the weaker report last month, the Fed chair Powell said this week that employment gains were on track and that is not necessary to seek blockbuster job gains going forward.

US stocks today moved higher across the board with the Dow industrial average leading the way thanks to Merck (+8.4%), Disney (+4.1%) and American Express (+3.8%). A look at the final numbers in the stock market shows:

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts