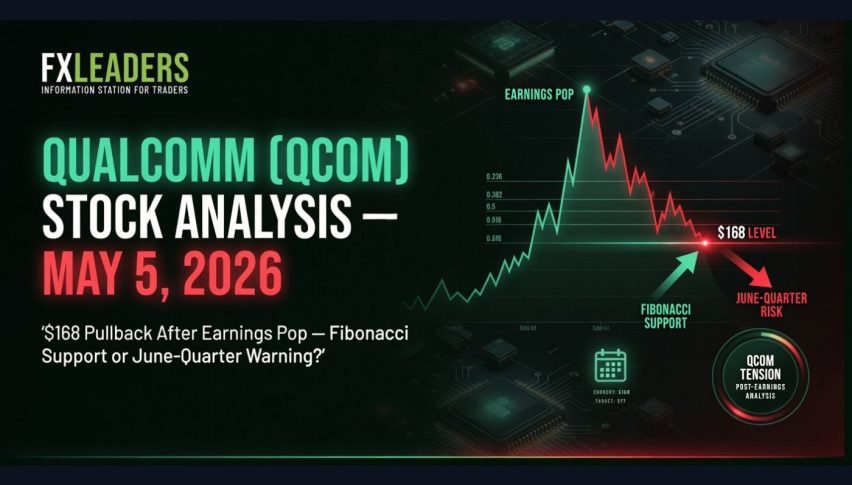

Qualcomm (QCOM) Stock Analysis — May 5, 2026: $168 Pullback After Earnings Pop — Fibonacci Support or June-Quarter Warning?

QCOM closed at $168.38 on May 4, down 4.88% for the day, after analysts raised concerns about weak Android demand affecting Q3 guidance.

Quick overview

- QCOM closed at $168.38 on May 4, down 4.88%, amid concerns about weak Android demand impacting Q3 guidance.

- Despite strong Q2 FY2026 results with $10.6 billion in revenue and record automotive revenue, analysts question the sustainability of growth.

- The stock is testing key support levels between $166 and $168, with potential buying opportunities suggested near this range.

- Long-term prospects remain positive, with a $45 billion design-win pipeline in automotive and a new $20 billion share repurchase plan.

QCOM closed at $168.38 on May 4, down 4.88% for the day, after analysts raised concerns about weak Android demand affecting Q3 guidance. The stock has dropped from its post-earnings high of $180.49 and is now testing the $166 to $168 range. Q2 FY2026 results were strong, with $10.6 billion in revenue, $2.65 EPS, and record automotive revenue of $1.33 billion. Now, investors are asking if this pullback is a buying chance or an early warning that Q3 guidance of $9.2 to $10.0 billion could fall short of expectations.

The earnings beat is clear, but Q3 guidance is in question

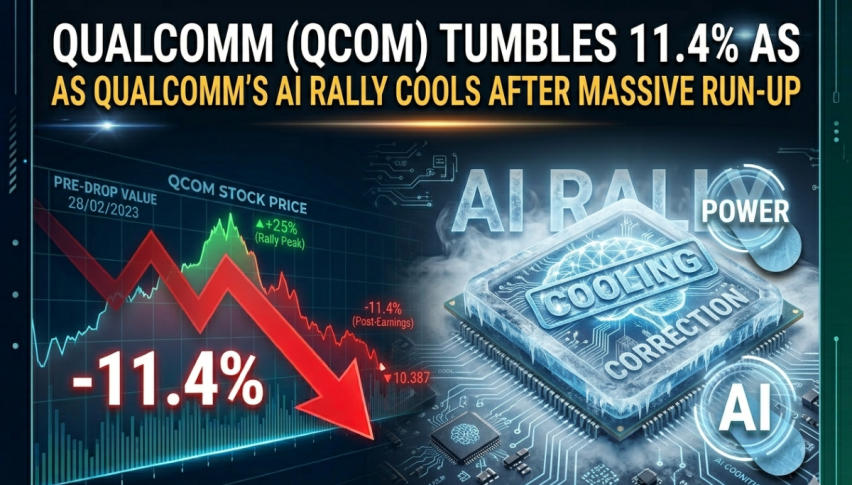

Q2 FY2026 revenue reached $10.60 billion, with non-GAAP EPS at $2.65, beating estimates by 3.67%. Automotive revenue hit a record $1.33 billion, up 38% from last year. IoT grew 9%, which helped balance out a 13% drop in handset sales caused by memory supply issues.

The main reason for Monday’s selloff is concern about the future. Analysts pointed out that Q3 revenue guidance of $9.2 to $10.0 billion suggests growth is slowing, especially with weak Android demand in China and ongoing memory pricing pressure. The handset segment, which is still Qualcomm’s biggest revenue source, dropped 13% in Q2 and there is no clear sign of a quick recovery.

The long-term positives for Qualcomm are still in place. The company confirmed a custom ASIC partnership with a major hyperscaler, calling it a multi-generation opportunity, with more details coming at AI Day in June. Qualcomm’s automotive business now has a $45 billion design-win pipeline. Its Snapdragon platforms are used in smartphones, PCs, and more vehicles, making Qualcomm an edge AI compute platform rather than just a handset chip supplier. The company also bought back $5.4 billion in shares in the first half of fiscal 2026 and approved a new $20 billion repurchase plan.

Trefis sets a long-term target of $340 for QCOM if revenue grows 15% each year to reach $65 billion by 2029. They also note that the stock trades at only 17 times forward earnings, while the broader semiconductor sector trades above 35 times. The June AI Day is expected to be the next big event for the stock.

QCOM Technical Analysis: $166 to $168 is the key support level

QCOM reached a high of $180.49 after earnings but has dropped 6.7% to $168.38 over two sessions. The stock is now testing the 0.618 Fibonacci retracement from the post-earnings move, with $166 to $168 as the main support area.

Support levels are at $166 to $168 (0.618 Fibonacci and current test), then $161 to $164 (deeper Fibonacci support), and $154 as the invalidation point. Resistance levels are at $171, then $177 (0.236 Fibonacci and previous resistance), and $205.95, which is the 52-week high.

The 50-period MA is rising and sits below current price — trend support intact. RSI rolling toward the mid-40s confirms cooling momentum, not reversal. The 200-period MA near $145 remains the broader structural floor.

Trade idea: Consider buying near the $166 to $168 support level, with targets at $171 and $177, and a stop below $161.

24/7 Wall St. has a target of $208.78 for QCOM. Trefis estimates fair value at $177. Analyst consensus ranges from $220 to $300.

FAQ: QCOM — Post-Earnings Pullback, Android Risk, and June AI Day

Why is Qualcomm stock falling after a strong earnings beat?

The Q2 beat is clear, with $2.65 EPS and record automotive revenue. The recent selloff is due to concerns about the future: Q3 guidance of $9.2 to $10.0 billion suggests slower growth, mainly because of weak Android demand in China and ongoing memory pricing pressure. After the stock hit $180 following earnings, the market had already expected strong results, so the cautious Q3 outlook gave investors a reason to take profits.

What is the Apple modem cliff and how real is the risk?

Apple is moving to its own modem, which could put about $7 billion of Qualcomm’s revenue at risk over time. These challenges are real, well-known, and already affecting the stock price. Now, the market is focusing on new opportunities: automotive revenue at a $6 billion run rate, the hyperscaler ASIC partnership, and the OpenAI smartphone chip project planned for 2028 production.

What is the Qualcomm price target for 2026?

24/7 Wall St. has a target of $208.78 for QCOM based on Q2 results, which suggests a 24% upside from the current price of $168. Trefis gives a base case of $177 and sees a long-term path to $340 if revenue grows 15% each year. The June AI Day, where Qualcomm will share more about the hyperscaler ASIC partnership, is the next big event for the stock. If Qualcomm secures steady data center revenue, it could close the valuation gap with Broadcom, which trades above 30 times forward earnings compared to Qualcomm’s 17 times.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts