Oracle (ORCL) Stock Analysis: $553B Backlog, AI Revenue Surge, and a $700B Bet on Cloud Infrastructure

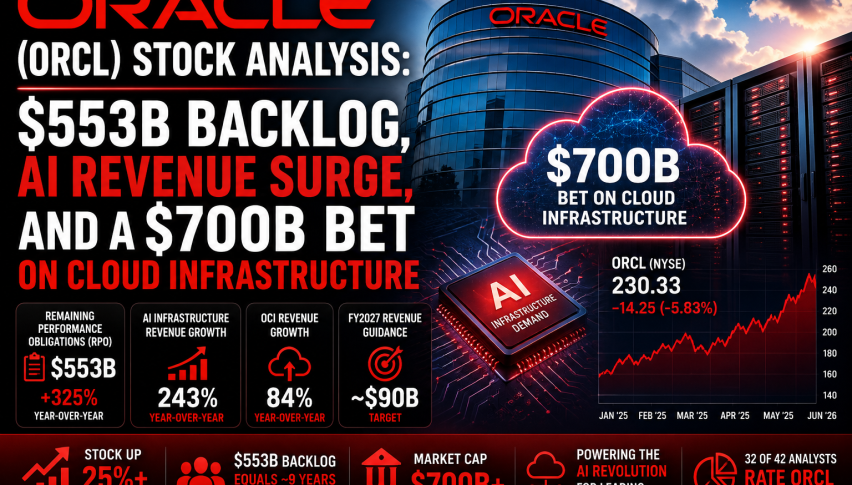

ORCL stock: Oracle holds a $553B backlog and targets AI-driven growth, but debt and AI spending remain key investor concerns.

Written by:

Arslan Ali Butt•Thursday, June 4, 2026•3 min read

•Last updated: Thursday, June 4, 2026

Quick overview

Oracle shares dropped nearly 6% on June 3, despite analysts raising price targets ahead of the June 10 earnings report.

The company has seen a significant rally, gaining approximately 45% over the past year, driven by its role in AI infrastructure.

Oracle faces challenges with rising debt and capital spending, as it must execute its ambitious growth plans effectively.

The upcoming earnings report is critical for determining if Oracle can convert its substantial backlog into profitable revenue.

Oracle shares fell nearly 6% on June 3, with additional weakness in after-hours trading, even as Wall Street analysts continue raising price targets ahead of the company’s June 10 earnings report.

The decline comes after a remarkable rally. Oracle has gained roughly 45% over the past year and surged nearly 28% in just one week as investors increasingly view the company as one of the largest beneficiaries of the global AI infrastructure buildout.

The key question facing investors is no longer demand.

It is execution.

Oracle now sits at the center of the AI data center race, serving customers such as OpenAI while competing against hyperscalers including Amazon, Microsoft, and Google. The company has amassed one of the largest contracted revenue backlogs in corporate history, but it must also spend aggressively to deliver that growth.

The Bull Case: Oracle’s $553 Billion Backlog Changes the Story

Oracle is no longer being valued primarily as a database company.

The investment narrative increasingly revolves around cloud infrastructure and AI.

Several numbers stand out:

Remaining Performance Obligations (RPO): $553 billion, up 325% year-over-year

Analysts believe Oracle has become one of the largest suppliers of AI infrastructure outside the traditional hyperscaler ecosystem.

The company’s relationships with OpenAI and other AI customers have fueled demand for massive GPU clusters and cloud computing capacity.

Recent partnerships and data center expansion efforts have further strengthened investor confidence.

Mizuho recently reiterated an Outperform rating and raised its price target to $320, citing confidence in Oracle’s execution and accelerating AI demand.

UBS also lifted its target to $285, pointing to continued momentum across Oracle’s cloud and AI businesses.

Of 42 analysts covering the stock, 32 currently rate Oracle a Buy.

The Bear Case for ORCL Stock: Debt, Capital Spending, and Execution Risk

The challenge is funding growth.

Oracle’s AI ambitions require unprecedented investment in data centers, networking equipment, and GPU infrastructure.

Several risks remain:

Non-current debt has risen to approximately $125 billion

Levered free cash flow remains negative

Oracle may require up to $50 billion in additional financing

Interest expense continues rising

OCI expansion depends heavily on successful execution

Morgan Stanley remains more cautious.

The firm maintains an Equal Weight rating and highlights several risks:

Slower OCI capacity deployment

Margin pressure from AI infrastructure investments

Customer concentration risk

Potential weakness in GPU-as-a-Service demand

The market increasingly wants evidence that Oracle can convert its massive backlog into profitable revenue rather than simply accumulating contracts.

Oracle’s June 10 Earnings Could Become a Major Catalyst

Options markets imply roughly a 12% move following earnings.

Historically, Oracle has frequently exceeded options-implied volatility around earnings announcements.

Investors will focus on:

FY2027 revenue outlook

OCI growth rates

AI infrastructure demand

Capital expenditure guidance

Free cash flow trajectory

Funding requirements

The biggest debate centers on whether Oracle can achieve management’s ambitious long-term targets without excessive shareholder dilution or debt issuance.

How to trade Oracle stock today

ORCL Technical Analysis: Uptrend Remains Intact, But Momentum Is Cooling

Technically, Oracle remains one of the strongest software and AI infrastructure charts in the market despite Wednesday’s pullback.

The stock recently approached all-time highs before investors locked in profits ahead of earnings.

Key Technical Signals

Shares remain up more than 25% year-to-date

Price trades above all major moving averages from the 10-day through 200-day

ADX at 34.6 confirms a strong established trend

VWMA at 207.2 remains well below current prices

Earnings anticipation has driven elevated trading volume

The broader trend remains bullish, although the stock appears extended after its recent surge.

RSI and MACD

Momentum indicators suggest Oracle may be entering a consolidation phase before its next major move.

The combination suggests momentum remains positive, but expectations have become elevated heading into earnings.

Key Support and Resistance Levels

Level Type

Approximate Area

Immediate Resistance

$245-$250

Major Resistance

$285-$320

Psychological Resistance

$350

Near-Term Support

$215-$220

Secondary Support

$200-$205

Major Trend Support

$185-$190

The $215-$220 zone represents the first important support area. Holding above it would preserve the current bullish structure.

Long-Term Outlook: Oracle Is Becoming an AI Infrastructure Giant

Oracle’s transformation is one of the most significant shifts in large-cap technology.

The company is moving beyond databases and enterprise software into AI infrastructure, cloud computing, and hyperscale data centers.

The opportunity is enormous.

Big Tech is expected to spend more than $700 billion on AI infrastructure this year, creating one of the largest technology investment cycles in decades.

However, investors are effectively betting that management can execute one of the largest data center expansion programs in corporate history while keeping debt and capital spending under control.

For now, the market appears willing to make that bet.

The June 10 earnings report could determine whether Oracle’s AI-fueled rally has another leg higher—or whether investors begin demanding proof that growth can eventually translate into sustainable free cash flow.

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Ali Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.