Why Dell is a Strong Buy After a Sudden $421 Pullback

Old-school hardware companies have shown they can best new-age tech firms in the race for AI gold. On June 4, 2026, Dell Technologies...

Quick overview

- Dell Technologies has outperformed newer tech firms in the AI sector, reporting record revenue of $43.8 billion for Q1 fiscal earnings.

- The company's backlog has reached an all-time high of $51.3 billion, driven by significant orders for AI-optimized servers.

- Despite recent stock fluctuations, analysts have raised price targets for Dell, with Goldman Sachs issuing a $500 target.

- Potential challenges include competitive pricing and supply chain bottlenecks amid a complex macroeconomic environment.

Old-school hardware companies have shown they can best new-age tech firms in the race for AI gold. On June 4, 2026, Dell Technologies (NYSE: DELL) shares were down 3.27% to trade around $421. The sell-off was brief after the stock hit an all-time high of $469 on June 1. Dig deeper though and there’s no reason for concern: on May 28, Dell (DEL) reported first-quarter fiscal earnings that smashed expectations, with record revenue of $43.8 billion, a massive 88% year over year. The impressive print has seen a host of Wall Street analysts raise their price targets on Dell, including a recent Goldman Sachs note reiterating a Buy and issuing a massive $500 target.

Driving the $51.3 Billion AI Backlog and Keeping Cool Amid Macro Red Flags

The Infrastructure Solutions Group, home to Dell’s PowerEdge servers, is driving growth. Through an alliance with Nvidia, Dell is manufacturing servers that are the backbone of the AI revolution. Hyperscalers and major corporations have lined up: Dell booked $24.4 billion worth of new AI-optimized server orders in one quarter alone.

Dell’s backlog has now climbed to an all-time high of $51.3 billion, while it also has a massive $9.7 billion defense contract for computing hardware that serves as an additional foundation. Management has confidently lifted its full-year guidance to a range of $165 billion to $169 billion, including a very healthy $60 billion in AI server revenues.

There are some caveats, though. Dell has to manage competitive pricing and a possible bottleneck in supply chains. The macro picture is also murky. In April, inflation was reported to be at a headline 3.8%, while the core rate was 4.1%. That kind of inflationary persistence has Fed Chair Kevin Warsh staying hawkish on interest rates, which could dampen spending by corporations in the future.

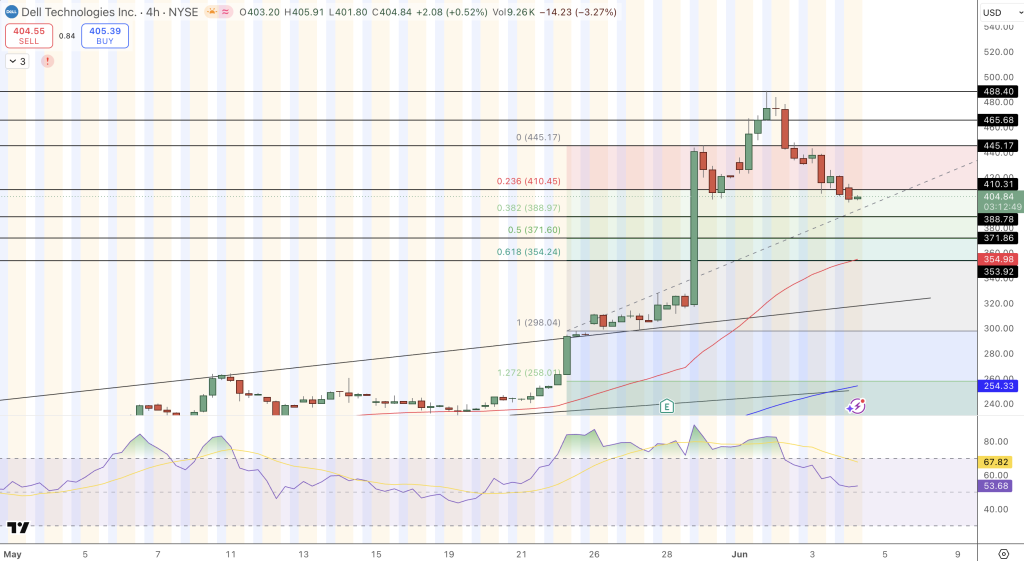

DELL Price Analysis: Charting the Optimal $404 Entry Point

On the 4-hour chart, Dell ($404.84) is in an optimal position to resume the uptrend that began in late April. The recent profit-taking has been controlled, as the stock has come back down to test the 0.236 Fibonacci level at $410.45. Dell (DEL) is still in its broader uptrend channel. It sits above the ascending black trendline that it’s been above since touching the $298 lows as well as the 0.382 Fibonacci level at $388.97.

Trading volume has been low on the red days, suggesting the recent pullback is just healthy institutional trimming. An ideal entry point can be at the current prices of $404.84 or once it breaks back through $410.45. Traders should place their stops just below $388.90 with the first stop target to $445.17.

In a nutshell, Dell’s fundamentals remain robust. For long-term investors looking for high-conviction opportunities on the path of the longer-term AI infrastructure build-out, this pullback is welcome.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts