Meta (META) Falls on AI Funding Fears Despite $56.3B Revenue Surge and $145B Capex Bet

Meta stock: Meta Platforms weighs stock sale to fund AI as revenue jumps 33% to $56.3 billion and capex guidance rises to $145 billion.

Written by:

Arslan Ali Butt•Tuesday, June 9, 2026•3 min read

•Last updated: Tuesday, June 9, 2026

Quick overview

Meta Platforms is experiencing a debate among investors regarding its significant capital expenditure increase to $145 billion for AI investments.

Despite strong revenue growth and advertising performance, concerns about potential stock dilution and the speed of AI returns are causing uncertainty.

Meta's AI initiatives are already showing positive results, with improved ad conversion rates and increased user engagement across its platforms.

Analysts remain optimistic about Meta's long-term prospects, citing strong fundamentals and a favorable valuation compared to peers.

Meta Platforms (NASDAQ: META) is facing a new investor debate.

The company continues to deliver some of the strongest operating results in Big Tech. Revenue growth has accelerated. Advertising performance remains robust. AI is already boosting monetization across Facebook, Instagram, WhatsApp, and Messenger.

Yet Wall Street remains focused on one issue: cost.

Meta’s decision to raise its 2026 capital expenditure guidance to as much as $145 billion has reignited concerns about whether AI investments will generate returns fast enough to justify the spending. Reports that the company may consider a multibillion-dollar stock sale to help finance its AI ambitions have added another layer of uncertainty.

With a market capitalization of roughly $1.5 trillion and shares trading around $585, investors are increasingly weighing near-term dilution risks against Meta’s long-term AI opportunity.

Meta’s AI Spending Is Reaching Historic Levels

Meta has become one of the world’s largest AI infrastructure investors.

Key figures include:

Q1 2026 revenue: $56.3 billion, up 33% year-over-year

Operating income growth: 30%

Q1 free cash flow: $12.4 billion

Long-term debt: approximately $59 billion

Recent senior notes issuance: $25 billion

2026 capex guidance: $125 billion to $145 billion

Management says demand for compute capacity continues to exceed expectations.

CFO Susan Li has repeatedly cited:

Rising memory costs

Expanding data center requirements

Growing AI training needs

Increased inference workloads

Combined spending by Meta, Alphabet, Microsoft, and Amazon is expected to exceed $720 billion in 2026, underscoring the scale of the AI arms race.

Why Investors Are Worried About a Potential META Stock Sale

Recent reports suggested Meta is exploring a potential equity raise worth tens of billions of dollars.

Meta has publicly denied that any formal plan exists, calling reports “pure speculation.”

Still, investors are taking the possibility seriously after Alphabet recently completed an approximately $85 billion equity offering to fund AI infrastructure.

A stock sale would provide capital without increasing debt, but it would also dilute existing shareholders.

The concern is not necessarily the dilution itself. Given Meta’s $1.5 trillion valuation, a raise worth several tens of billions would likely represent low-single-digit dilution.

The bigger question is whether AI investments ultimately generate sufficient returns.

Reality Labs remains a cautionary example. The division posted another roughly $4 billion quarterly operating loss, extending cumulative losses to approximately $83 billion since 2020.

AI Is Already Improving Meta’s Core Business

While investors focus on spending, Meta argues AI is already producing measurable results.

According to management:

AI ad models increased conversion rates for landing-page ads by more than 6%

Generative AI video tools improved advertiser conversion rates by more than 3%

Meta’s AI-powered value optimization suite now exceeds a $20 billion annual revenue run rate

Weekly conversations with business AI agents have increased 10-fold since the start of the year

CEO Mark Zuckerberg continues pushing toward what he describes as “personal superintelligence.”

However, investors may not need to wait for futuristic AI assistants to justify the spending.

Meta’s advertising machine remains the key driver.

Advertising impressions increased 19% in the latest quarter, while average price per ad rose 12%, both significantly above year-earlier levels.

Analysts Continue to Back Meta’s Long-Term Story

Despite recent volatility, many analysts remain constructive.

Several investors point to Meta’s valuation relative to other Magnificent Seven companies.

Highlights include:

Forward P/E near 22x

Revenue growth of 33%

Operating margin of 41%

Nearly 4 billion monthly active users across Meta’s platforms

Gene Munster noted that engagement metrics remain strong and that Meta’s latest AI initiatives are already increasing user activity across Facebook and Instagram.

Other analysts argue Meta remains one of the few companies clearly demonstrating tangible returns from AI spending today.

How to trade the dip in Meta stock

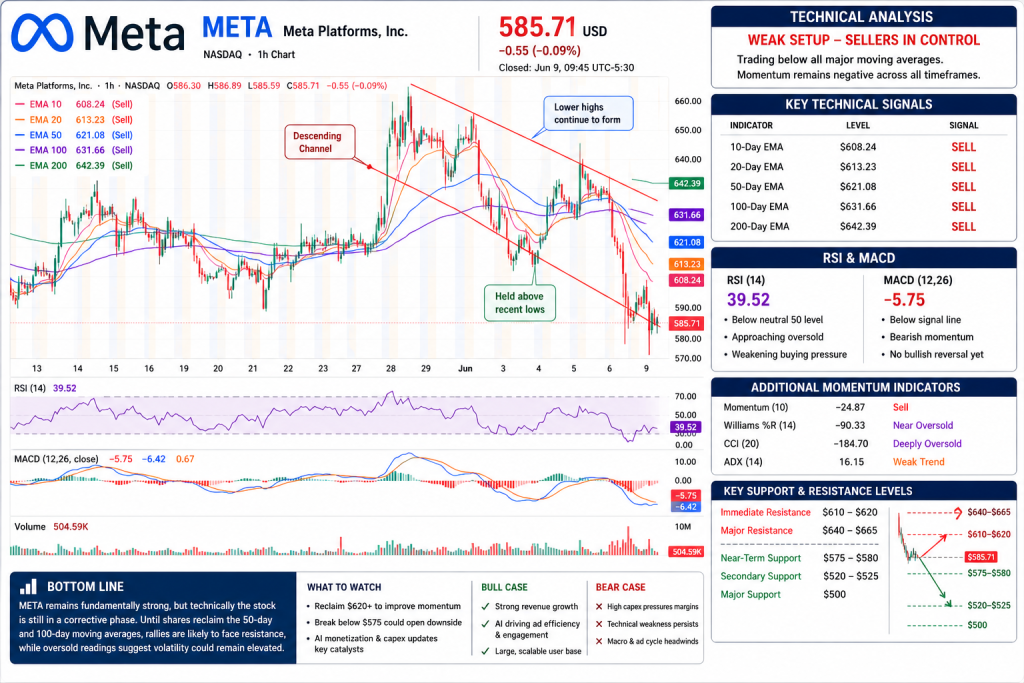

META Technical Analysis: AI Optimism Meets Funding Concerns

Meta’s technical setup has weakened materially in recent weeks.

The stock is trading below all major moving averages, indicating sellers remain in control despite strong fundamental performance and AI-driven revenue growth.

Key Technical Signals

Indicator

Level

Signal

10-Day EMA

$608.24

Sell

20-Day EMA

$613.23

Sell

50-Day EMA

$621.08

Sell

100-Day EMA

$631.66

Sell

200-Day EMA

$642.39

Sell

META now trades below its 10-, 20-, 50-, 100-, and 200-day moving averages. This bearish alignment confirms that momentum remains negative across short-, medium-, and long-term timeframes.

RSI and MACD

RSI: 39.52

Below neutral 50 level

Approaching oversold territory

Reflects weakening buying pressure

MACD: -5.75

Remains below the signal line

Bearish momentum persists

No confirmed bullish reversal yet

Key Support and Resistance Levels

Level Type

Approximate Area

Immediate Resistance

$610-$620

Major Resistance

$640-$665

Near-Term Support

$575-$580

Secondary Support

$520-$525

Major Support

$500

A recovery above the $620 area would be the first sign that buyers are regaining control. Conversely, a break below $575 could increase pressure toward the $520-$525 support zone.

Bottom line: META remains fundamentally strong, but technically the stock is still in a corrective phase. Until shares reclaim the 50-day and 100-day moving averages, rallies are likely to face resistance, while oversold readings suggest volatility could remain elevated.

Long-Term Outlook: One of the Largest AI Bets in Corporate History

Meta’s investment thesis increasingly revolves around AI.

The company is spending at a pace rarely seen in corporate history. Critics argue the returns remain uncertain. Supporters counter that AI is already improving advertising performance, engagement, and monetization.

The next 12 to 24 months will likely determine whether Meta’s AI spending becomes a landmark success or another expensive moonshot.

For now, the fundamentals remain strong.

Revenue is accelerating. Margins remain among the highest in Big Tech. The advertising business continues to generate enormous cash flow.

The challenge is proving that a $145 billion infrastructure buildout can create enough future value to justify today’s spending. Investors appear willing to wait for that answer—but not indefinitely.

Lead Markets Analyst – Multi-Asset (FX, Commodities, Crypto)

Arslan Ali Butt serves as the Lead Commodities and Indices Analyst, bringing a wealth of expertise to the field. With an MBA in Behavioral Finance and active progress towards a Ph.D., Arslan possesses a deep understanding of market dynamics.

His professional journey includes a significant role as a senior analyst at a leading brokerage firm, complementing his extensive experience as a market analyst and day trader. Adept in educating others, Arslan has a commendable track record as an instructor and public speaker.

His incisive analyses, particularly within the realms of cryptocurrency and forex markets, are showcased across esteemed financial publications such as ForexCrunch, InsideBitcoins, and EconomyWatch, solidifying his reputation in the financial community.