Apple (AAPL) Stock Analysis: $289 After Record Q2 — Memory Cost Headwind and WWDC Are the Two Stories That Matter

AAPL closed at $289.74 on May 7, rising 6% since the April 30 Q2 earnings report, which was Apple’s best March quarter yet. Revenue...

Quick overview

- AAPL closed at $289.74 on May 7, marking a 6% increase since the April 30 Q2 earnings report, which revealed record revenue of $111.2 billion.

- Despite a 22% year-over-year increase in iPhone revenue to $57 billion, it fell short of analyst expectations due to supply constraints.

- Apple anticipates significantly higher memory costs in Q3, impacting product gross margins, but maintains a strong growth outlook of 14 to 17% for the upcoming quarter.

- The company has approved an additional $100 billion for share buybacks and raised its quarterly dividend by 4%, reflecting confidence in its financial strategy.

AAPL closed at $289.74 on May 7, rising 6% since the April 30 Q2 earnings report, which was Apple’s best March quarter yet. Revenue hit $111.2 billion, up 17% from last year. EPS came in at $2.01, beating estimates by $0.06. The Q3 growth outlook of 14 to 17% is well above the 9.5% analyst consensus. There’s plenty of reason for optimism ahead of WWDC, though Tim Cook’s warning about higher memory costs is still important.

The One Caveat in an Otherwise Exceptional Quarter

iPhone revenue was $57 billion, up 22% from last year, but it came in just below analyst expectations. This was the only number in the report that missed. Cook said the shortfall was due to supply constraints, since Apple is competing for TSMC’s 3nm chips and dealing with high demand for AI infrastructure. This is a long-term issue that won’t be fixed quickly.

Cook said Apple expects “significantly higher memory costs” in Q3 and beyond. Product gross margin has already fallen by 200 basis points to 38.7%, mostly due to higher memory prices and seasonal trends. The global memory shortage, caused by strong AI server demand, is now pushing up Apple’s costs and could get worse. The Services gross margin of 76.7% helps, but lower product margins are still a real challenge for now.

There are strong positives too. Greater China revenue rose 28% to $20.5 billion, bouncing back from last year’s weakness and showing the iPhone 17 cycle is strong in this market. Apple approved another $100 billion for share buybacks and raised its quarterly dividend by 4% to $0.27. The company has already repurchased $37 billion in shares in the first half of FY2026, keeping up its record capital returns. The Q3 growth outlook of 14 to 17%, compared to the 9.5% consensus, is the most optimistic part of the report.

It’s also worth noting that Apple spent only $4.3 billion on capital expenditures in the first half of FY2026. That’s a big difference from Amazon, Meta, and Google, who have each committed over $100 billion to AI infrastructure. Apple’s AI strategy is centered on software and on-device intelligence, not building more data centers. This approach helps keep free cash flow available for buybacks and dividends.

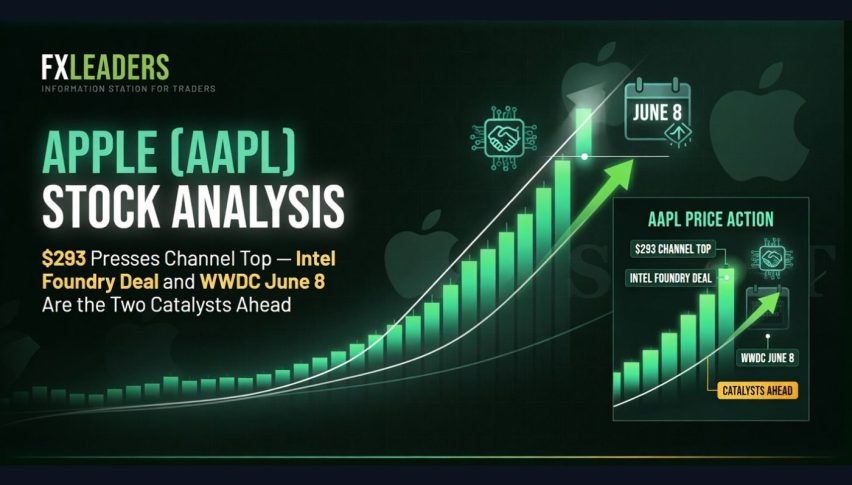

AAPL Technical Analysis: Channel Upper Boundary at $290.58

On the 2-hour chart, AAPL is testing the top of a steep rising channel that began at the mid-April lows near $269. A doji pattern at the 1.0 Fibonacci extension ($287.26) shows the market is deciding whether to move higher or pull back toward the middle of the channel.

Resistance: $290.58 (1.272 Fibonacci) → $294.77 (1.618 Fibonacci).

Support: $285.17 (immediate cluster) → $280.77 (channel midline / red MA) → $277.97–$279.74 (0.236–0.382 Fibonacci zone).

The RSI is between 66 and 69, which is a healthy level. It’s high but not overbought, so there’s still room for more gains if the price moves above the $290.58 resistance with strong volume.

Trade setup: Long above $288.50 | Target $290.58–$294.77 | Stop below $285.17.

FAQ: AAPL — Memory Cost Risk, WWDC Catalyst, and the CEO Transition

What is the memory cost headwind and how serious is it for Apple?

Apple’s product gross margin fell 200 basis points sequentially to 38.7% in Q2, and Cook warned of “significantly higher memory costs” in Q3 and beyond. The global memory shortage is driven by AI server demand competing for the same DRAM and NAND supply Apple uses in iPhones and Macs. At Apple’s $111 billion quarterly revenue scale, each 100 basis points of product gross margin represents approximately $500 million in quarterly gross profit — material but manageable given Services margins at 76.7%.

What should investors watch at WWDC 2026 on June 8–12?

The two questions that move the stock: first, whether Siri 2.0 and Apple Intelligence upgrades deliver the agentic AI capabilities needed to drive an iPhone 18 upgrade cycle among the installed base of 2.5 billion active devices; second, whether Apple announces any monetisation model for premium AI features — an Apple Intelligence subscription or tiered pricing would be the first evidence that the Services franchise is expanding into AI, which is the key re-rating argument at 28–29x forward earnings.

What does Tim Cook’s CEO transition mean for Apple’s stock?

Cook is in his final year as CEO before transitioning to executive chairman, with John Ternus expected to take the top role. Ternus, Apple’s current hardware engineering chief, led the Apple Silicon transition — the most successful product platform shift in Apple’s post-Jobs era. Markets are pricing this as continuity rather than risk. The Q3 guidance beat and $100 billion buyback authorisation reinforce the message that strategy is not changing.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts