Nvidia NVDA Stock Tests $200 Level Again as Valuation Fears and Geopolitical Risks Intensify

Even as rising pricing, geopolitical volatility, and growing concerns about valuation continue to put pressure on investors, NVIDIA...

Quick overview

- NVIDIA reported strong Q1 FY27 earnings with $81.6 billion in revenue, driven by high demand for AI infrastructure and advanced computing systems.

- Despite impressive growth, rising operating expenses and geopolitical tensions, particularly regarding China, are causing investor sentiment to weaken.

- The Data Center division was the main growth driver, contributing $75.2 billion in revenue, while gross margins remained high at 74.9%.

- NVIDIA is attempting to bolster investor confidence through significant buybacks and increased dividends, but faces challenges from rising costs and market uncertainties.

Rising pricing, geopolitical volatility, and growing concerns about valuation continue to put pressure on investors, NVIDIA delivered another outstanding profits quarter driven by the relentless demand for chips from AI itself because consumers aren’t using them.

Another Explosive Quarter for NVIDIA

NVIDIA once again reported blockbuster quarterly results as global demand for artificial intelligence infrastructure and advanced computing systems remained exceptionally strong. The company continues to dominate the AI semiconductor landscape, benefiting from aggressive spending by hyperscale cloud providers and large-scale data center operators.

For Q1 FY27, NVIDIA generated revenue of $81.6 billion, representing a 20% increase from the previous quarter and an 85% surge year-over-year. The results reinforced the company’s central role in the ongoing AI investment boom, where demand for high-performance GPUs and networking hardware continues accelerating globally.

The Data Center division remained the primary growth engine, contributing $75.2 billion in revenue as enterprises and cloud providers expanded AI infrastructure deployment at an aggressive pace. Gross margins remained elevated at 74.9%, while diluted earnings per share reached $2.39, highlighting the company’s continued pricing power despite mounting competition.

Rising Costs Begin Clouding the Outlook

Despite the headline strength, investor sentiment weakened as markets increasingly focused on the rapidly rising cost structure supporting NVIDIA’s expansion. Operating expenses climbed to $7.6 billion during the quarter as the company accelerated research spending, infrastructure investment, and product development efforts to maintain its technological lead.

Tax expenses also surged sharply to $11.6 billion, while investing cash outflows reached $26.4 billion as NVIDIA continued pouring capital into next-generation AI systems and semiconductor platforms. Although operating cash flow remained exceptionally strong at $50.3 billion, investors appear increasingly concerned that the company’s historically efficient profitability profile may face growing pressure as spending intensifies.

The reaction reflects a broader concern across the technology sector that even dominant AI leaders may struggle to maintain margin expansion indefinitely during aggressive investment cycles.

China Restrictions Add Long-Term Uncertainty

Another growing overhang remains the ongoing geopolitical tension surrounding semiconductor exports to China. NVIDIA management indicated that it expects no meaningful Data Center compute revenue from China during Q2 due to continuing export restrictions and regulatory barriers.

The absence of one of the world’s largest semiconductor markets raises concerns about future growth flexibility and increases dependence on a relatively concentrated group of hyperscale customers in North America and other regions. The restrictions also create uncertainty around long-term valuation assumptions, particularly as investors question how sustainable current growth rates may remain over time.

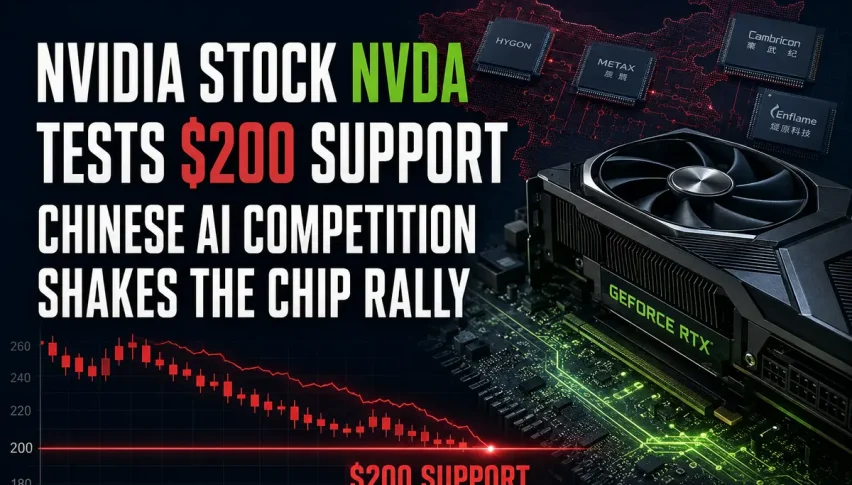

Technical Picture Reflects Waning Momentum

Nvidia’s technical setup mirrors the shifting sentiment. The stock slipped to its 20-day simple moving average (gray) in early May, but reversed back up, so it provided reliable support and NVDA reached a new high of $236 last week before earnings. But then the stock reversed down and now sellers are testing the 20 SMA again. If it breaks, we will likely see a deeper pullback to $200.

NVDA Chart Daily – Heading to $200

Buybacks Support Confidence but Risks Persist

NVIDIA attempted to reinforce confidence by returning roughly $20 billion to shareholders through dividends and share repurchases during the quarter. The company also approved an additional $80 billion buyback authorization and raised its quarterly dividend to $0.25 per share.

Even so, the stock remains under pressure and continues trading below recent highs as investors weigh extraordinary growth against rising costs, geopolitical instability, execution risks, and increasingly stretched valuation expectations across the semiconductor sector.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts