Meta Platforms (META) Stock Analysis: $610 Falling Wedge Base After Earnings Drop — Can the $145B AI Bet Pay Off?

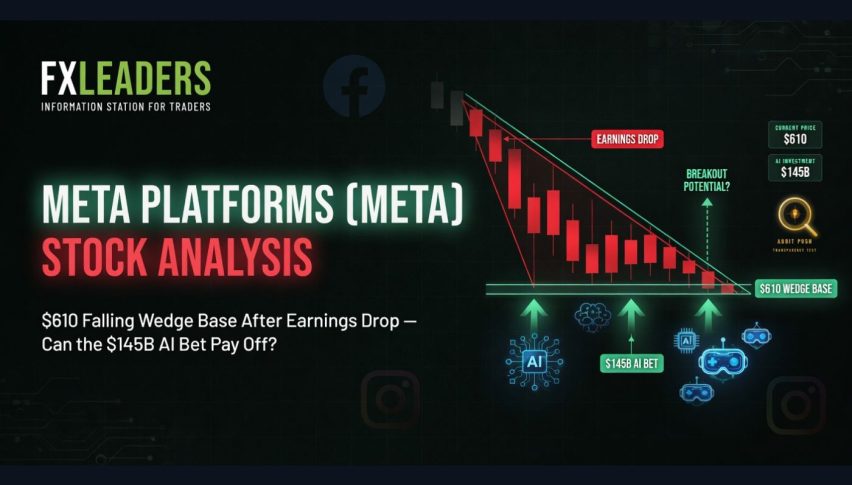

META closed at $610.41 on May 4, bouncing back from an early 7–10% drop after Q1 FY2026 results showed 33% revenue growth but also raised...

Quick overview

- META closed at $610.41 on May 4, recovering from a 7–10% drop after reporting a 33% revenue growth in Q1 FY2026.

- The company raised its 2026 capex guidance to $125–145 billion, nearly double its 2025 spending, raising concerns among investors.

- Despite strong ad performance, including a 19% increase in ad impressions, there are challenges such as user drops linked to geopolitical issues in Iran.

- Analysts have set a price target for META between $750 and $882.71, suggesting potential growth despite current market concerns.

META closed at $610.41 on May 4, bouncing back from an early 7–10% drop after Q1 FY2026 results showed 33% revenue growth but also raised 2026 capex guidance to $125–145 billion, almost double 2025’s spending. The stock is now testing support at $600, near the lower edge of a falling wedge pattern. The story is straightforward: Meta’s ad business is strong, but the big question is whether the $145 billion AI investment is smart or too much.

The Numbers: A Clean Beat With One Asterisk

In Q1 2026, revenue grew 33% year-over-year to $56.31 billion, net income rose 61% to $26.77 billion, and diluted EPS climbed 62% to $10.44. The ad business stood out, with ad impressions across the Family of Apps up 19% and the average price per ad up 12%. This strong performance shows that AI targeting improvements are making a real impact.

There is an important detail: EPS included an $8.03 billion income tax benefit from the One Big Beautiful Bill Act. Without this, diluted EPS would have been $3.13 lower. Adjusted EPS was $7.31, which still beat the $6.79 consensus, but the headline $10.44 figure overstates the company’s real earnings power. Investors should focus on the $7.31 adjusted number for Q1.

There were two more negatives from the call. Meta said a drop in users was partly due to “internet disruptions in Iran,” a new geopolitical challenge linked to the Hormuz conflict that is affecting user engagement in the Middle East. Management also confirmed plans to cut the employee base in May, showing a focus on cost control as capex rises.

The $145 Billion Question

Meta’s 2026 capex guidance of $125–145 billion is almost twice the $72.2 billion spent in 2025, and it is more than what Meta spent in 2025 and 2024 combined. The CFO said the increase is due to higher component prices and extra data center costs for future capacity, not a shift in strategy.

CFO Susan Li said the adaptive ranking model led to a 1.6% increase in conversion rates, and the value optimisation suite now brings in over $20 billion in annual revenue. This shows that AI spending is already delivering real returns in the ad business. Claims that capex is “unproven” overlook this clear result.

For Q2 2026, Meta expects revenue between $58 and $61 billion. The midpoint, $59.5 billion, suggests about 25% year-over-year growth, which is slower than Q1’s 33%. This slowdown is a real short-term challenge.

24/7 Wall St. has set a price target of $882.71. They believe that the market is mispricing Meta by punishing the stock despite 33% revenue growth, rather than seeing it as a warning sign.

META Technical Analysis: Falling Wedge at $600 Support

After earnings, the stock dropped and formed a falling wedge pattern from the $742 high. This pattern usually ends with a bullish move when the price reaches the tip of the wedge.

The 0.618 Fibonacci retracement from the 2025 peak is at $610, which acts as a support level. The price is staying close to the lower channel boundary around $600–$610, while the red moving average at $636–$650 is the next resistance above.

Support levels are at $600 (trendline), then $580, and $550–$560 in a bearish scenario. Resistance is at $636–$650 (gap fill and moving average), then $670, and above $700. The The RSI is in the middle range and shows no strong divergence, which suggests a stable or slightly positive base instead of a move lower.

Trade idea: Go long if the daily close is above $620, aim for a target of $650, and set a stop below $600.

FAQ: META — Capex Concern, Iran User Impact, and the Path to $700+

Why did Meta stock drop on a 33% revenue beat?

The selloff happened because Meta raised capex to $125–145 billion, almost double 2025’s spending and higher than analyst estimates of $122.6 billion. Free cash flow will stay tight in the near term, since $19.84 billion per quarter in infrastructure spending will use up much of the operating cash. Investors worry that revenue growth may not keep up with this level of spending.

How does the Iran conflict affect Meta’s business?

Meta pointed to “internet disruptions in Iran” as a reason for slower user growth in Q1. This is a direct result of the Strait of Hormuz crisis and the US blockade, which have hurt internet infrastructure in the region. Since Meta operates at a large scale, changes in Middle Eastern user engagement are noticeable. If the conflict continues into Q2, this challenge will likely remain.

What is the Meta stock price target for 2026?

Analysts expect Meta’s stock to reach $750 to $830 over the next 12 months, which would be a 23–36% gain from $610. 24/7 Wall St. has a higher target of $882.71, based on the idea that AI monetisation will keep growing. Technically, a close above $620 could fill the $636–$650 gap, and a strong move above $670 could push the stock to $700–$750 by mid-2026. The next big events are Q2 earnings in late July and any updates on AI agent product launches.

- Check out our free forex signals

- Follow the top economic events on FX Leaders economic calendar

- Trade better, discover more Forex Trading Strategies

- Open a FREE Trading Account

- Read our latest reviews on: Avatrade, Exness, HFM and XM

Related Articles

Sidebar rates

Related Posts